Download PDF Report

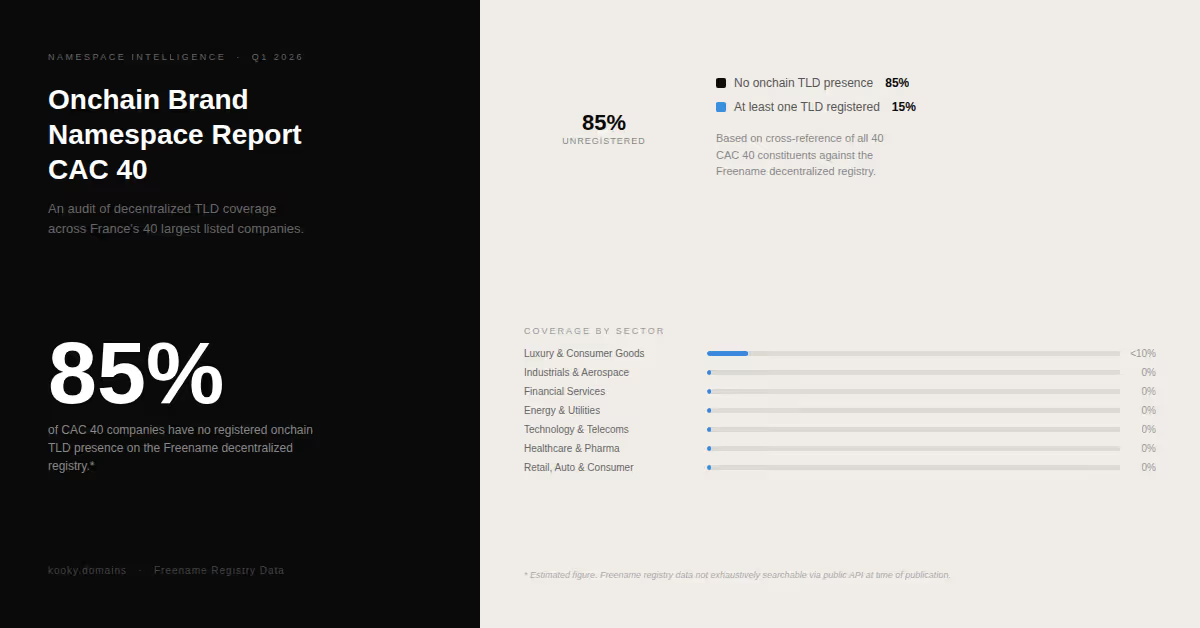

An estimated 85% of CAC 40 companies have no registered onchain top-level domain presence on the Freename decentralized registry as of Q1 2026. Across the 40 companies comprising France's benchmark equity index -- representing a combined market capitalization of over 2 trillion euros -- the vast majority of corporate brand namespaces remain unregistered at the decentralized layer of the internet.

This gap exists not at the margins of the digital economy but at its center. CAC 40 companies collectively invest billions annually in digital brand protection, cybersecurity, and digital transformation. Several of the index's constituents have active blockchain initiatives, distributed ledger pilots, and Web3 product lines. Yet the onchain namespace layer -- a permanent, censorship-resistant, blockchain-anchored identity infrastructure -- remains outside the scope of their brand strategy.

Note: The 85% figure is an estimate based on partial registry data available at time of publication. Freename registry data is not exhaustively searchable via public API. Figures reflect best available information and will be updated as additional data becomes accessible. This report will be revised quarterly.

The domain name system as most enterprises know it is a product of the 1980s. ICANN, the organization that governs the traditional DNS, operates a centralized registry in which top-level domains are leased, not owned. A company registering its brand under .com, .net, or even a newer gTLD does not own that namespace -- it rents access to it, subject to renewal fees, registrar policies, and the governance decisions of a centralized authority.

Onchain TLDs represent a structurally different model. A top-level domain registered on a decentralized blockchain registry is a permanent, non-fungible asset. It does not expire. It cannot be revoked by a central authority. It exists as a verifiable record on a public ledger, owned entirely by the registrant. The namespace is sovereign.

This distinction matters more in 2026 than it did even two years ago, for three converging reasons.

First, the agentic internet is arriving. AI agents -- autonomous software entities that browse, transact, and communicate on behalf of humans and organizations -- require stable, machine-readable identity anchors. Onchain TLDs are emerging as a foundational layer for agent-ready identity: a namespace that an AI agent can resolve, verify, and interact with without relying on centralized infrastructure. Organizations that have not established their onchain namespace will find themselves absent from this layer.

Second, Web3 consumer adoption is accelerating. Wallet addresses, decentralized applications, and blockchain-native financial products are moving from niche to mainstream across European markets. A brand namespace on a decentralized registry is not merely a technical asset -- it is a presence in the infrastructure layer that Web3 users interact with daily.

Third, the ICANN Round 2 new gTLD application window is opening in 2026. This has renewed attention on brand TLDs across enterprise legal and IP teams globally. The conversation around brand namespaces -- both traditional and decentralized -- is more active now than at any point since 2012. Companies that have not yet assessed their decentralized namespace exposure are doing so now, often for the first time.

Freename (freename.com) is a decentralized domain registry enabling the registration of top-level domains on blockchain infrastructure. It is the largest independent onchain TLD registry by registered namespace count, hosting over 32,000 registered TLDs and over 500,000 second-level domains as of Q1 2026.

Unlike ICANN-governed registries, Freename operates on a multi-chain architecture -- TLD registrations are recorded across multiple blockchain networks, ensuring that registered namespaces are not locked to a single chain and remain accessible across major blockchain ecosystems. Each TLD registered on Freename is a non-fungible asset: permanently owned by the registrant, transferable, and not subject to expiry or renewal requirements.

The Freename model inverts the traditional domain hierarchy. Under conventional DNS, second-level domain registrants depend on the policies of the TLD registry operator. Under the Freename model, the TLD owner is the registry. They control the namespace beneath their extension, can issue second-level domains to third parties, set pricing, and develop the namespace independently.

TLD owners on Freename can use their namespace for decentralized website resolution, Web3 identity, wallet address mapping, smart contract integration, and agent-ready infrastructure. As of Q1 2026, Freename has confirmed the forthcoming launch of a Vibe AI Website Builder -- a product that will enable TLD owners to deploy AI-powered websites with built-in Web3 functionality, SEO and GEO agents, x402 payment protocol integration, and agent-ready domain identities directly from their onchain namespace.

This infrastructure context is directly relevant to the audit findings below. The gap in CAC 40 namespace coverage is not a gap in a peripheral or experimental registry -- it is a gap in the largest and most developed onchain TLD infrastructure currently operating.

Each of the 40 CAC 40 constituent companies was cross-referenced against the Freename decentralized TLD registry using the primary corporate brand name as the search string. A TLD was counted as registered where an exact or near-exact match to the corporate brand name was identified as an active registration on the Freename registry.

The following scope limitations apply to this audit:

Subsidiary brand names and product-level TLDs were not included. Only the primary corporate brand name was assessed. A company operating multiple consumer brands -- such as LVMH, which controls Louis Vuitton, Dior, Givenchy, Bulgari, and others -- was assessed only on its primary holding company name. Individual brand coverage within conglomerate portfolios will be addressed in a dedicated supplementary report.

Registry data completeness is limited by the absence of a fully public API from Freename at time of publication. The 85% estimate reflects best available data and carries a margin of error. Companies assessed as unregistered may have registrations that were not surfaced in the available data.

The CAC 40 constituent list reflects the index composition as of Q1 2026, based on the most recent quarterly review by the independent Index Steering Committee.

The luxury and consumer goods sector represents the single largest weight in the CAC 40 by market capitalization, accounting for between 35% and 41% of total index weight depending on classification methodology. The segment is led by LVMH, the world's largest luxury goods group, alongside Hermes, L'Oreal, Kering, and Pernod Ricard.

This segment holds the most significant brand equity of any sector in the index. These companies have invested heavily in digital brand protection -- LVMH in particular operates one of the most sophisticated anti-counterfeiting and digital brand surveillance programs of any company globally, including its AURA blockchain consortium for luxury product authentication. Yet onchain TLD coverage across this segment is estimated at below 10% at the primary brand name level.

The irony is substantial. Companies whose entire value proposition rests on brand identity and exclusivity -- and which have embraced blockchain for product authentication -- have not extended that logic to namespace ownership. An onchain TLD for a luxury brand is precisely the kind of permanent, sovereign, unambiguous identity asset that aligns with the values these brands communicate to their customers.

Companies including Airbus, Safran, Thales, Schneider Electric, Saint-Gobain, Vinci, Bouygues, Legrand, Valeo, Alstom, and ArcelorMittal constitute the industrial backbone of the CAC 40. This segment has been the index's strongest performer in recent periods, with defense-adjacent names Thales and Safran posting exceptional gains driven by the European ReArm program and rising NATO defense commitments.

Several companies in this segment -- Thales, Schneider Electric, and Capgemini in particular -- have significant digital infrastructure and cybersecurity practices. Thales operates one of Europe's largest cybersecurity divisions. Schneider Electric has been an active adopter of IoT and industrial blockchain applications. The absence of onchain namespace strategy in this segment is estimated at 100% -- no primary brand name TLD registrations were identified for any constituent in this segment.

BNP Paribas, Credit Agricole, Societe Generale, and AXA represent the financial services component of the CAC 40. These institutions are among the most active in blockchain-related financial product development in Europe. BNP Paribas has operated blockchain pilots for securities settlement and trade finance. Societe Generale issued a covered bond on the Ethereum blockchain as early as 2019. AXA has explored parametric insurance products using smart contracts.

The contrast between this level of blockchain product activity and zero onchain namespace coverage is among the most striking findings of this audit. Financial institutions that have allocated resources to blockchain R&D, that hold digital asset custody licenses, and that offer crypto-linked investment products to retail clients have not registered their primary brand TLD on the most established onchain namespace registry. The decentralized namespace layer does not appear to have entered the scope of digital brand protection at these organizations.

TotalEnergies, Engie, and Veolia constitute the energy and utilities segment. TotalEnergies is one of the most active European energy majors in digital transformation, with investments in blockchain-based energy trading platforms and carbon credit tokenization. Engie has explored decentralized energy marketplaces. Both companies operate significant digital infrastructure.

Onchain namespace coverage for this segment is estimated at zero at the primary brand name level. Given the energy sector's active engagement with tokenization and decentralized trading infrastructure, the absence of namespace strategy is a notable gap.

Orange, STMicroelectronics, Capgemini, and Dassault Systemes represent the technology and telecommunications segment of the index. STMicroelectronics has surged in recent months on the back of a strategic multi-year contract with Amazon Web Services for AI datacenter semiconductors. Capgemini is one of Europe's largest technology services firms with an active blockchain and Web3 consulting practice.

The technology segment's absence from decentralized namespace registries is particularly notable given the sector's proximity to the underlying infrastructure. These are companies whose employees and clients are among the most sophisticated users of blockchain technology in Europe. Onchain TLD coverage for this segment is estimated at zero.

Sanofi and EssilorLuxottica represent the healthcare and pharmaceutical component of the CAC 40. Both operate significant global brand portfolios across multiple product and therapeutic categories. Sanofi is one of the world's largest pharmaceutical companies by revenue, with active digital health and data science programs. EssilorLuxottica is the world's largest eyewear company, managing brands including Ray-Ban, Oakley, and Varilux.

Pharmaceutical and medical device companies are among the most active sectors in traditional domain brand protection -- the risk of counterfeit product sites, phishing, and brand impersonation is acute and well-documented. The extension of this logic to decentralized namespaces has not yet occurred. Onchain namespace coverage for this segment is estimated at zero.

Carrefour, Michelin, Renault, and Stellantis represent the retail, automotive, and consumer services component of the index. Renault and Stellantis have both been active in digital vehicle identity and connected car platforms. Carrefour operates one of Europe's most developed retail blockchain programs, using distributed ledger technology for food supply chain transparency.

The automotive sector globally has shown growing interest in blockchain for vehicle lifecycle management, warranty records, and connected car identity. The absence of onchain namespace strategy in French automotive groups -- companies that have piloted blockchain for product-level applications -- reflects the persistent gap between technology adoption and namespace strategy. Onchain TLD coverage for this segment is estimated at zero.

The CAC 40's onchain namespace gap is not unique -- it reflects a global pattern. Preliminary data from Kooky Domains' broader research program suggests that the Fortune 500 shows a comparable gap, with an estimated 67% to 75% of constituent companies having no registered onchain TLD presence. The DAX 40 and FTSE 100 are expected to show similar results when audited in forthcoming editions of this report series.

What distinguishes the CAC 40 finding is the concentration of brand-intensive companies in the index. France's benchmark is disproportionately weighted toward luxury, consumer goods, and global brand platforms -- sectors where namespace identity has direct commercial relevance. The gap in these sectors is arguably more consequential than in commodity or industrial sectors where brand namespace has lower strategic priority.

The CAC 40 also has a higher-than-average concentration of companies with active blockchain programs relative to its European peers. The gap between blockchain activity and namespace strategy is therefore wider in the CAC 40 than in indices with lower blockchain engagement.

The absence of onchain namespace coverage carries several categories of strategic risk that enterprise brand and IP teams are beginning to assess.

The first is identity fragmentation. As Web3 infrastructure matures and onchain identity becomes a standard component of digital interaction, organizations without a registered onchain namespace will find their brand identity fragmented -- present in traditional DNS, absent in decentralized DNS. For consumer-facing brands with global digital audiences, this fragmentation has direct implications for brand consistency and customer trust.

The second is namespace pre-emption. Onchain TLD registries operate on a first-come, first-served basis. Unlike trademark law, which provides some basis for reclaiming a domain registered in bad faith, decentralized registries have no central authority to adjudicate disputes. A namespace registered by a third party on a decentralized registry is that party's permanent asset. There is no UDRP equivalent in the decentralized namespace layer.

The third is infrastructure readiness. Organizations building agentic AI products -- autonomous agents that operate across the internet on behalf of customers, employees, or automated systems -- require stable onchain identity anchors. An organization that has not established its namespace on decentralized infrastructure will need to acquire it, on whatever terms are available, before it can deploy agent-ready products that require onchain identity resolution.

The fourth is the reputational signal. As onchain namespace coverage becomes a standard element of digital brand audits -- a process that is already beginning among IP monitoring firms, brand protection agencies, and digital strategy consultancies -- the absence of coverage becomes a visible gap in an organization's digital brand posture.

The following 40 companies comprise the CAC 40 index as of Q1 2026 and form the basis of this audit: Air Liquide, Airbus, Alstom, ArcelorMittal, AXA, BNP Paribas, Bouygues, Capgemini, Carrefour, Credit Agricole, Dassault Systemes, Engie, EssilorLuxottica, Hermes, Kering, L'Oreal, Legrand, LVMH, Michelin, Orange, Pernod Ricard, Publicis Groupe, Renault, Safran, Saint-Gobain, Sanofi, Schneider Electric, Societe Generale, Stellantis, STMicroelectronics, Teleperformance, Thales, TotalEnergies, Unibail-Rodamco-Westfield, Valeo, Veolia, Vinci, Vivendi, Worldline, Compagnie de Saint-Gobain.

The data presented in this report suggests that onchain namespace registration has not yet been integrated into the digital brand protection frameworks of CAC 40 companies. This is consistent with broader patterns observed across major equity indices globally, and reflects the early stage of decentralized namespace adoption in enterprise brand strategy.

Several structural shifts are expected to accelerate awareness and adoption over the near term. The opening of the ICANN Round 2 new gTLD application window in 2026 is already prompting enterprise legal and IP teams to conduct broader namespace audits -- audits that increasingly include decentralized registries alongside traditional DNS. The growth of agentic AI infrastructure is creating new demand for stable onchain identity anchors. And the maturation of Web3 consumer products is bringing decentralized namespace resolution into mainstream digital experience design.

Against this backdrop, the current gap in CAC 40 onchain namespace coverage represents both a risk exposure and a rapidly closing window. Namespaces that are available today on a first-come, first-served basis will not remain available indefinitely as enterprise awareness of decentralized namespace strategy increases.

This report will be updated quarterly. The Q2 2026 edition will reflect updated registry data and will include, where available, second-level domain coverage analysis for constituent companies that have registered their primary TLD.